Third eye • StrategyThird eye • Strategy – User Guide

1. Idea & Concept

Third eye • Strategy combines three things into one system:

Ichimoku Cloud – to define market regime and support/resistance.

Moving Average (trend filter) – to trade only in the dominant direction.

CCI (Commodity Channel Index) – to generate precise entry signals on momentum breakouts.

The script is a strategy, not an indicator: it can backtest entries, exits, SL, TP and BreakEven logic automatically.

2. Indicators Used

2.1 Ichimoku

Standard Ichimoku settings (by default 9/26/52/26) are used:

Conversion Line (Tenkan-sen)

Base Line (Kijun-sen)

Leading Span A & B (Kumo Cloud)

Lagging Span is calculated but hidden from the chart (for visual simplicity).

From the cloud we derive:

kumoTop – top of the cloud under current price.

kumoBottom – bottom of the cloud under current price.

Flags:

is_above_kumo – price above the cloud.

is_below_kumo – price below the cloud.

is_in_kumo – price inside the cloud.

These conditions are used as trend / regime filters and for stop-loss & trailing stops.

2.2 Moving Average

You can optionally display and use a trend MA:

Types: SMA, EMA, DEMA, WMA

Length: configurable (default 200)

Source: default close

Filter idea:

If MA Direction Filter is ON:

When Close > MA → strategy allows only Long signals.

When Close < MA → strategy allows only Short signals.

The MA is plotted on the chart (if enabled).

2.3 CCI & Panel

The CCI (Commodity Channel Index) is used for entry timing:

CCI length and source are configurable (default length 20, source hlc3).

Two thresholds:

CCI Upper Threshold (Long) – default +100

CCI Lower Threshold (Short) – default –100

Signals:

Long signal:

CCI crosses up through the upper threshold

cci_val < upper_threshold and cci_val > upper_threshold

Short signal:

CCI crosses down through the lower threshold

cci_val > lower_threshold and cci_val < lower_threshold

There is a panel (table) in the bottom-right corner:

Shows current CCI value.

Shows filter status as colored dots:

Green = filter enabled and passed.

Red = filter enabled and blocking trades.

Gray = filter is disabled.

Filters shown in the panel:

Ichimoku Cloud filter (Long/Short)

Ichimoku Lines filter (Conversion/Base vs Cloud)

MA Direction filter

3. Filters & Trade Direction

All filters can be turned ON/OFF independently.

3.1 Ichimoku Cloud Filter

Purpose: trade only when price is clearly above or below the Kumo.

Long Cloud Filter (Use Ichimoku Cloud Filter) – when enabled:

Long trades only if close > cloud top.

Short Cloud Filter – when enabled:

Short trades only if close < cloud bottom.

If the cloud filter is disabled, this condition is ignored.

3.2 Ichimoku Lines Above/Below Cloud

Purpose: stronger trend confirmation: Ichimoku lines should also be on the “correct” side of the cloud.

Long Lines Filter:

Long allowed only if Conversion Line and Base Line are both above the cloud.

Short Lines Filter:

Short allowed only if both lines are below the cloud.

If this filter is OFF, the conditions are not checked.

3.3 MA Direction Filter

As described above:

When ON:

Close > MA → only Longs.

Close < MA → only Shorts.

4. Anti-Re-Entry Logic (Cloud Touch Reset)

The strategy uses internal flags to avoid continuous re-entries in the same direction without a reset.

Two flags:

allowLong

allowShort

After a Long entry, allowLong is set to false, allowShort to true.

After a Short entry, allowShort is set to false, allowLong to true.

Flags are reset when price touches the Kumo:

If Low goes into the cloud → allowLong = true

If High goes into the cloud → allowShort = true

If Close is inside the cloud → both allowLong and allowShort are set to true

There is a key option:

Wait Position Close Before Flag Reset

If ON: cloud touch will reset flags only when there is no open position.

If OFF: flags can be reset even while a trade is open.

This gives a kind of regime-based re-entry control: after a trend leg, you wait for a “cloud interaction” to allow new signals.

5. Risk Management

All risk management is handled inside the strategy.

5.1 Position Sizing

Order Size % of Equity – default 10%

The strategy calculates:

position_value = equity * (Order Size % / 100)

position_qty = position_value / close

So position size automatically adapts to your current equity.

5.2 Take Profit Modes

You can choose one of two TP modes:

Percent

Fibonacci

5.2.1 Percent Mode

Single Take Profit at X% from entry (default 2%).

For Long:

TP = entry_price * (1 + tp_pct / 100)

For Short:

TP = entry_price * (1 - tp_pct / 100)

One strategy.exit per side is used: "Long TP/SL" and "Short TP/SL".

5.2.2 Fibonacci Mode (2 partial TPs)

In this mode, TP levels are based on a virtual Fib-style extension between entry and stop-loss.

Inputs:

Fib TP1 Level (default 1.618)

Fib TP2 Level (default 2.5)

TP1 Share % (Fib) (default 50%)

TP2 share is automatically 100% - TP1 share.

Process for Long:

Compute a reference Stop (see SL section below) → sl_for_fib.

Compute distance: dist = entry_price - sl_for_fib.

TP levels:

TP1 = entry_price + dist * (Fib TP1 Level - 1)

TP2 = entry_price + dist * (Fib TP2 Level - 1)

For Short, the logic is mirrored.

Two exits are used:

TP1 – closes TP1 share % of position.

TP2 – closes remaining TP2 share %.

Same stop is used for both partial exits.

5.3 Stop-Loss Modes

You can choose one of three Stop Loss modes:

Stable – fixed % from entry.

Ichimoku – fixed level derived from the Kumo.

Ichimoku Trailing – dynamic SL following the cloud.

5.3.1 Stable SL

For Long:

SL = entry_price * (1 - Stable SL % / 100)

For Short:

SL = entry_price * (1 + Stable SL % / 100)

Used both for Percent TP mode and as reference for Fib TP if Kumo is not available.

5.3.2 Ichimoku SL (fixed, non-trailing)

At the time of a new trade:

For Long:

Base SL = cloud bottom minus small offset (%)

For Short:

Base SL = cloud top plus small offset (%)

The offset is configurable: Ichimoku SL Offset %.

Once computed, that SL level is fixed for this trade.

5.3.3 Ichimoku Trailing SL

Similar to Ichimoku SL, but recomputed each bar:

For Long:

SL = cloud bottom – offset

For Short:

SL = cloud top + offset

A red trailing SL line is drawn on the chart to visualize current stop level.

This trailing SL is also used as reference for BreakEven and for Fib TP distance.

6. BreakEven Logic (with BE Lines)

BreakEven is optional and supports two modes:

Percent

Fibonacci

Inputs:

Percent mode:

BE Trigger % (from entry) – move SL to BE when price goes this % in profit.

BE Offset % from entry – SL will be set to entry ± this offset.

Fibonacci mode:

BE Fib Level – Fib level at which BE will be activated (default 1.618, same style as TP).

BE Offset % from entry – how far from entry to place BE stop.

The logic:

Before BE is triggered, SL follows its normal mode (Stable/Ichimoku/Ichimoku Trailing).

When BE triggers:

For Long:

New SL = max(current SL, BE SL).

For Short:

New SL = min(current SL, BE SL).

This means BE will never loosen the stop – only tighten it.

When BE is activated, the strategy draws a violet horizontal line at the BreakEven level (once per trade).

BE state is cleared when the position is closed or when a new position is opened.

7. Entry & Exit Logic (Summary)

7.1 Long Entry

Conditions for a Long:

CCI signal:

CCI crosses up through the upper threshold.

Ichimoku Cloud Filter (optional):

If enabled → price must be above the Kumo.

Ichimoku Lines Filter (optional):

If enabled → Conversion Line and Base Line must be above the Kumo.

MA Direction Filter (optional):

If enabled → Close must be above the chosen MA.

Anti-re-entry flag:

allowLong must be true (cloud-based reset).

Position check:

Long entries are allowed when current position size ≤ 0 (so it can also reverse from short to long).

If all these conditions are true, the strategy sends:

strategy.entry("Long", strategy.long, qty = calculated_qty)

After entry:

allowLong = false

allowShort = true

7.2 Short Entry

Same structure, mirrored:

CCI signal:

CCI crosses down through the lower threshold.

Cloud filter: price must be below cloud (if enabled).

Lines filter: conversion & base must be below cloud (if enabled).

MA filter: Close must be below MA (if enabled).

allowShort must be true.

Position check: position size ≥ 0 (allows reversal from long to short).

Then:

strategy.entry("Short", strategy.short, qty = calculated_qty)

Flags update:

allowShort = false

allowLong = true

7.3 Exits

While in a position:

The strategy continuously recalculates SL (depending on chosen mode) and, in Percent mode, TP.

In Fib mode, fixed TP levels are computed at entry.

BreakEven may raise/tighten the SL if its conditions are met.

Exits are executed via strategy.exit:

Percent mode: one TP+SL exit per side.

Fib mode: two partial exits (TP1 and TP2) sharing the same SL.

At position open, the script also draws visual lines:

White line — entry price.

Green line(s) — TP level(s).

Red line — SL (if not using Ichimoku Trailing; with trailing, the red line is updated dynamically).

Maximum of 30 lines are kept to avoid clutter.

8. How to Use the Strategy

Choose market & timeframe

Works well on trending instruments. Try crypto, FX or indices on H1–H4, or intraday if you prefer more trades.

Adjust Ichimoku settings

Keep defaults (9/26/52/26) or adapt to your timeframe.

Configure Moving Average

Typical: EMA 200 as a trend filter.

Turn MA Direction Filter ON if you want to trade only with the main trend.

Set CCI thresholds

Default ±100 is classic.

Lower thresholds → more signals, higher noise.

Higher thresholds → fewer but stronger signals.

Enable/disable filters

Turn on Ichimoku Cloud and Ichimoku Lines if you want only “clean” trend trades.

Use Wait Position Close Before Flag Reset to control how often re-entries are allowed.

Choose TP & SL mode

Percent mode is simpler and easier to understand.

Fibonacci mode is more advanced: it aligns TP levels with the distance to stop, giving asymmetric RR setups (two partial TPs).

Choose Stable SL for fixed-risk trades, or Ichimoku / Ichimoku Trailing to tie stops to the cloud structure.

Set BreakEven

Enable BE if you want to lock in risk-free trades after a certain move.

Percent mode is straightforward; Fib mode keeps BreakEven in harmony with your Fib TP setup.

Run Backtest & Optimize

Press “Add to chart” → go to Strategy Tester.

Adjust parameters to your market and timeframe.

Look at equity curve, PF, drawdown, average trade, etc.

Live / Paper Trading

After you’re satisfied with backtest results, use the strategy to generate signals.

You can mirror entries/exits manually or connect them to alerts (if you build an alert-based execution layer).

Cari dalam skrip untuk "the strat"

Prop Firm Business SimulatorThe prop firm business simulator is exactly what it sounds like. It's a plug and play tool to test out any tradingview strategy and simulate hypothetical performance on CFD Prop Firms.

Now what is a modern day CFD Prop Firm?

These companies sell simulated trading challenges for a challenge fee. If you complete the challenge you get access to simulated capital and you get a portion of the profits you make on those accounts payed out.

I've included some popular firms in the code as presets so it's easy to simulate them. Take into account that this info will likely be out of date soon as these prices and challenge conditions change.

Also, this tool will never be able to 100% simulate prop firm conditions and all their rules. All I aim to do with this tool is provide estimations.

Now why is this tool helpful?

Most traders on here want to turn their passion into their full-time career, prop firms have lately been the buzz in the trading community and market themselves as a faster way to reach that goal.

While this all sounds great on paper, it is sometimes hard to estimate how much money you will have to burn on challenge fees and set realistic monthly payout expectations for yourself and your trading. This is where this tool comes in.

I've specifically developed this for traders that want to treat prop firms as a business. And as a business you want to know your monthly costs and income depending on the trading strategy and prop firm challenge you are using.

How to use this tool

It's quite simple you remove the top part of the script and replace it with your own strategy. Make sure it's written in same version of pinescript before you do that.

//--$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$--//--------------------------------------------------------------------------------------------------------------------------$$$$$$

//--$$$$$--Strategy-- --$$$$$$--// ******************************************************************************************************************************

//--$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$--//--------------------------------------------------------------------------------------------------------------------------$$$$$$

length = input.int(20, minval=1, group="Keltner Channel Breakout")

mult = input(2.0, "Multiplier", group="Keltner Channel Breakout")

src = input(close, title="Source", group="Keltner Channel Breakout")

exp = input(true, "Use Exponential MA", display = display.data_window, group="Keltner Channel Breakout")

BandsStyle = input.string("Average True Range", options = , title="Bands Style", display = display.data_window, group="Keltner Channel Breakout")

atrlength = input(10, "ATR Length", display = display.data_window, group="Keltner Channel Breakout")

esma(source, length)=>

s = ta.sma(source, length)

e = ta.ema(source, length)

exp ? e : s

ma = esma(src, length)

rangema = BandsStyle == "True Range" ? ta.tr(true) : BandsStyle == "Average True Range" ? ta.atr(atrlength) : ta.rma(high - low, length)

upper = ma + rangema * mult

lower = ma - rangema * mult

//--Graphical Display--// *-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-$$$$$$

u = plot(upper, color=#2962FF, title="Upper", force_overlay=true)

plot(ma, color=#2962FF, title="Basis", force_overlay=true)

l = plot(lower, color=#2962FF, title="Lower", force_overlay=true)

fill(u, l, color=color.rgb(33, 150, 243, 95), title="Background")

//--Risk Management--// *-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-$$$$$$

riskPerTradePerc = input.float(1, title="Risk per trade (%)", group="Keltner Channel Breakout")

le = high>upper ? false : true

se = lowlower

strategy.entry('PivRevLE', strategy.long, comment = 'PivRevLE', stop = upper, qty=riskToLots)

if se and upper>lower

strategy.entry('PivRevSE', strategy.short, comment = 'PivRevSE', stop = lower, qty=riskToLots)

The tool will then use the strategy equity of your own strategy and use this to simulat prop firms. Since these CFD prop firms work with different phases and payouts the indicator will simulate the gains until target or max drawdown / daily drawdown limit gets reached. If it reaches target it will go to the next phase and keep on doing that until it fails a challenge.

If in one of the phases there is a reward for completing, like a payout, refund, extra it will add this to the gains.

If you fail the challenge by reaching max drawdown or daily drawdown limit it will substract the challenge fee from the gains.

These gains are then visualised in the calendar so you can get an idea of yearly / monthly gains of the backtest. Remember, it is just a backtest so no guarantees of future income.

The bottom pane (non-overlay) is visualising the performance of the backtest during the phases. This way u can check if it is realistic. For instance if it only takes 1 bar on chart to reach target you are probably risking more than the firm wants you to risk. Also, it becomes much less clear if daily drawdown got hit in those high risk strategies, the results will be less accurate.

The daily drawdown limit get's reset every time there is a new dayofweek on chart.

If you set your prop firm preset setting to "'custom" the settings below that are applied as your prop firm settings. Otherwise it will use one of the template by default it's FTMO 100K.

The strategy I'm using as an example in this script is a simple Keltner Channel breakout strategy. I'm using a 0.05% commission per trade as that is what I found most common on crypto exchanges and it's close to the commissions+spread you get on a cfd prop firm. I'm targeting a 1% risk per trade in the backtest to try and stay within prop firm boundaries of max 1% risk per trade.

Lastly, the original yearly and monthly performance table was developed by Quantnomad and I've build ontop of that code. Here's a link to the original publication:

That's everything for now, hope this indicator helps people visualise the potential of prop firms better or to understand that they are not a good fit for their current financial situation.

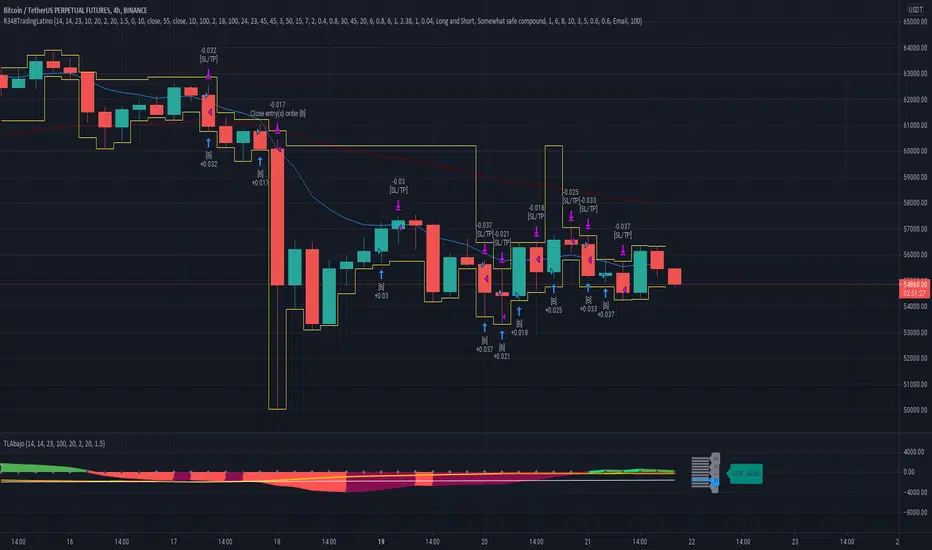

Ruckard TradingLatinoThis strategy tries to mimic TradingLatino strategy.

The current implementation is beta.

Si hablas castellano o espanyol por favor consulta MENSAJE EN CASTELLANO más abajo.

It's aimed at BTCUSDT pair and 4h timeframe.

STRATEGY DEFAULT SETTINGS EXPLANATION

max_bars_back=5000 : This is a random number of bars so that the strategy test lasts for one or two years

calc_on_order_fills=false : To wait for the 4h closing is too much. Try to check if it's worth entering a position after closing one. I finally decided not to recheck if it's worth entering after an order is closed. So it is false.

calc_on_every_tick=false

pyramiding=0 : We only want one entry allowed in the same direction. And we don't want the order to scale by error.

initial_capital=1000 : These are 1000 USDT. By using 1% maximum loss per trade and 7% as a default stop loss by using 1000 USDT at 12000 USDT per BTC price you would entry with around 142 USDT which are converted into: 0.010 BTC . The maximum number of decimal for contracts on this BTCUSDT market is 3 decimals. E.g. the minimum might be: 0.001 BTC . So, this minimal 1000 amount ensures us not to entry with less than 0.001 entries which might have happened when using 100 USDT as an initial capital.

slippage=1 : Binance BTCUSDT mintick is: 0.01. Binance slippage: 0.1 % (Let's assume). TV has an integer slippage. It does not have a percentage based slippage. If we assume a 1000 initial capital, the recommended equity is 142 which at 11996 USDT per BTC price means: 0.011 BTC. The 0.1% slippage of: 0.011 BTC would be: 0.000011 . This is way smaller than the mintick. So our slippage is going to be 1. E.g. 1 (slippage) * 0.01 (mintick)

commission_type=strategy.commission.percent and commission_value=0.1 : According to: binance . com / en / fee / schedule in VIP 0 level both maker and taker fees are: 0.1 %.

BACKGROUND

Jaime Merino is a well known Youtuber focused on crypto trading

His channel TradingLatino

features monday to friday videos where he explains his strategy.

JAIME MERINO STANCE ON BOTS

Jaime Merino stance on bots (taken from memory out of a 2020 June video from him):

'~

You know. They can program you a bot and it might work.

But, there are some special situations that the bot would not be able to handle.

And, I, as a human, I would handle it. And the bot wouldn't do it.

~'

My long term target with this strategy script is add as many

special situations as I can to the script

so that it can match Jaime Merino behaviour even in non normal circumstances.

My alternate target is learn Pine script

and enjoy programming with it.

WARNING

This script might be bigger than other TradingView scripts.

However, please, do not be confused because the current status is beta.

This script has not been tested with real money.

This is NOT an official strategy from Jaime Merino.

This is NOT an official strategy from TradingLatino . net .

HOW IT WORKS

It basically uses ADX slope and LazyBear's Squeeze Momentum Indicator

to make its buy and sell decisions.

Fast paced EMA being bigger than slow paced EMA

(on higher timeframe) advices going long.

Fast paced EMA being smaller than slow paced EMA

(on higher timeframe) advices going short.

It finally add many substrats that TradingLatino uses.

SETTINGS

__ SETTINGS - Basics

____ SETTINGS - Basics - ADX

(ADX) Smoothing {14}

(ADX) DI Length {14}

(ADX) key level {23}

____ SETTINGS - Basics - LazyBear Squeeze Momentum

(SQZMOM) BB Length {20}

(SQZMOM) BB MultFactor {2.0}

(SQZMOM) KC Length {20}

(SQZMOM) KC MultFactor {1.5}

(SQZMOM) Use TrueRange (KC) {True}

____ SETTINGS - Basics - EMAs

(EMAS) EMA10 - Length {10}

(EMAS) EMA10 - Source {close}

(EMAS) EMA55 - Length {55}

(EMAS) EMA55 - Source {close}

____ SETTINGS - Volume Profile

Lowest and highest VPoC from last three days

is used to know if an entry has a support

VPVR of last 100 4h bars

is also taken into account

(VP) Use number of bars (not VP timeframe): Uses 'Number of bars {100}' setting instead of 'Volume Profile timeframe' setting for calculating session VPoC

(VP) Show tick difference from current price {False}: BETA . Might be useful for actions some day.

(VP) Number of bars {100}: If 'Use number of bars (not VP timeframe)' is turned on this setting is used to calculate session VPoC.

(VP) Volume Profile timeframe {1 day}: If 'Use number of bars (not VP timeframe)' is turned off this setting is used to calculate session VPoC.

(VP) Row width multiplier {0.6}: Adjust how the extra Volume Profile bars are shown in the chart.

(VP) Resistances prices number of decimal digits : Round Volume Profile bars label numbers so that they don't have so many decimals.

(VP) Number of bars for bottom VPOC {18}: 18 bars equals 3 days in suggested timeframe of 4 hours. It's used to calculate lowest session VPoC from previous three days. It's also used as a top VPOC for sells.

(VP) Ignore VPOC bottom advice on long {False}: If turned on it ignores bottom VPOC (or top VPOC on sells) when evaluating if a buy entry is worth it.

(VP) Number of bars for VPVR VPOC {100}: Number of bars to calculate the VPVR VPoC. We use 100 as Jaime once used. When the price bounces back to the EMA55 it might just bounce to this VPVR VPoC if its price it's lower than the EMA55 (Sells have inverse algorithm).

____ SETTINGS - ADX Slope

ADX Slope

help us to understand if ADX

has a positive slope, negative slope

or it is rather still.

(ADXSLOPE) ADX cut {23}: If ADX value is greater than this cut (23) then ADX has strength

(ADXSLOPE) ADX minimum steepness entry {45}: ADX slope needs to be 45 degrees to be considered as a positive one.

(ADXSLOPE) ADX minimum steepness exit {45}: ADX slope needs to be -45 degrees to be considered as a negative one.

(ADXSLOPE) ADX steepness periods {3}: In order to avoid false detection the slope is calculated along 3 periods.

____ SETTINGS - Next to EMA55

(NEXTEMA55) EMA10 to EMA55 bounce back percentage {80}: EMA10 might bounce back to EMA55 or maybe to 80% of its complete way to EMA55

(NEXTEMA55) Next to EMA55 percentage {15}: How much next to the EMA55 you need to be to consider it's going to bounce back upwards again.

____ SETTINGS - Stop Loss and Take Profit

You can set a default stop loss or a default take profit.

(STOPTAKE) Stop Loss % {7.0}

(STOPTAKE) Take Profit % {2.0}

____ SETTINGS - Trailing Take Profit

You can customize the default trailing take profit values

(TRAILING) Trailing Take Profit (%) {1.0}: Trailing take profit offset in percentage

(TRAILING) Trailing Take Profit Trigger (%) {2.0}: When 2.0% of benefit is reached then activate the trailing take profit.

____ SETTINGS - MAIN TURN ON/OFF OPTIONS

(EMAS) Ignore advice based on emas {false}.

(EMAS) Ignore advice based on emas (On closing long signal) {False}: Ignore advice based on emas but only when deciding to close a buy entry.

(SQZMOM) Ignore advice based on SQZMOM {false}: Ignores advice based on SQZMOM indicator.

(ADXSLOPE) Ignore advice based on ADX positive slope {false}

(ADXSLOPE) Ignore advice based on ADX cut (23) {true}

(STOPTAKE) Take Profit? {false}: Enables simple Take Profit.

(STOPTAKE) Stop Loss? {True}: Enables simple Stop Loss.

(TRAILING) Enable Trailing Take Profit (%) {True}: Enables Trailing Take Profit.

____ SETTINGS - Strategy mode

(STRAT) Type Strategy: 'Long and Short', 'Long Only' or 'Short Only'. Default: 'Long and Short'.

____ SETTINGS - Risk Management

(RISKM) Risk Management Type: 'Safe', 'Somewhat safe compound' or 'Unsafe compound'. ' Safe ': Calculations are always done with the initial capital (1000) in mind. The maximum losses per trade/day/week/month are taken into account. ' Somewhat safe compound ': Calculations are done with initial capital (1000) or a higher capital if it increases. The maximum losses per trade/day/week/month are taken into account. ' Unsafe compound ': In each order all the current capital is gambled and only the default stop loss per order is taken into account. That means that the maximum losses per trade/day/week/month are not taken into account. Default : 'Somewhat safe compound'.

(RISKM) Maximum loss per trade % {1.0}.

(RISKM) Maximum loss per day % {6.0}.

(RISKM) Maximum loss per week % {8.0}.

(RISKM) Maximum loss per month % {10.0}.

____ SETTINGS - Decimals

(DECIMAL) Maximum number of decimal for contracts {3}: How small (3 decimals means 0.001) an entry position might be in your exchange.

EXTRA 1 - PRICE IS IN RANGE indicator

(PRANGE) Print price is in range {False}: Enable a bottom label that indicates if the price is in range or not.

(PRANGE) Price range periods {5}: How many previous periods are used to calculate the medians

(PRANGE) Price range maximum desviation (%) {0.6} ( > 0 ): Maximum positive desviation for range detection

(PRANGE) Price range minimum desviation (%) {0.6} ( > 0 ): Mininum negative desviation for range detection

EXTRA 2 - SQUEEZE MOMENTUM Desviation indicator

(SQZDIVER) Show degrees {False}: Show degrees of each Squeeze Momentum Divergence lines to the x-axis.

(SQZDIVER) Show desviation labels {False}: Whether to show or not desviation labels for the Squeeze Momentum Divergences.

(SQZDIVER) Show desviation lines {False}: Whether to show or not desviation lines for the Squeeze Momentum Divergences.

EXTRA 3 - VOLUME PROFILE indicator

WARNING: This indicator works not on current bar but on previous bar. So in the worst case it might be VP from 4 hours ago. Don't worry, inside the strategy calculus the correct values are used. It's just that I cannot show the most recent one in the chart.

(VP) Print recent profile {False}: Show Volume Profile indicator

(VP) Avoid label price overlaps {False}: Avoid label prices to overlap on the chart.

EXTRA 4 - ZIGNALY SUPPORT

(ZIG) Zignaly Alert Type {Email}: 'Email', 'Webhook'. ' Email ': Prepare alert_message variable content to be compatible with zignaly expected email content format. ' Webhook ': Prepare alert_message variable content to be compatible with zignaly expected json content format.

EXTRA 5 - DEBUG

(DEBUG) Enable debug on order comments {False}: If set to true it prepares the order message to match the alert_message variable. It makes easier to debug what would have been sent by email or webhook on each of the times an order is triggered.

HOW TO USE THIS STRATEGY

BOT MODE: This is the default setting.

PROPER VOLUME PROFILE VIEWING: Click on this strategy settings. Properties tab. Make sure Recalculate 'each time the order was run' is turned off.

NEWBIE USER: (Check PROPER VOLUME PROFILE VIEWING above!) You might want to turn on the 'Print recent profile {False}' setting. Alternatively you can use my alternate realtime study: 'Resistances and supports based on simplified Volume Profile' but, be aware, it might consume one indicator.

ADVANCED USER 1: Turn on the 'Print price is in range {False}' setting and help us to debug this subindicator. Also help us to figure out how to include this value in the strategy.

ADVANCED USER 2: Turn on the all the (SQZDIVER) settings and help us to figure out how to include this value in the strategy.

ADVANCED USER 3: (Check PROPER VOLUME PROFILE VIEWING above!) Turn on the 'Print recent profile {False}' setting and report any problem with it.

JAIME MERINO: Just use the indicator as it comes by default. It should only show BUY signals, SELL signals and their associated closing signals. From time to time you might want to check 'ADVANCED USER 2' instructions to check that there's actually a divergence. Check also 'ADVANCED USER 1' instructions for your amusement.

EXTRA ADVICE

It's advised that you use this strategy in addition to these two other indicators:

* Squeeze Momentum Indicator

* ADX

so that your chart matches as close as possible to TradingLatino chart.

ZIGNALY INTEGRATION

This strategy supports Zignaly email integration by default. It also supports Zignaly Webhook integration.

ZIGNALY INTEGRATION - Email integration example

What you would write in your alert message:

||{{strategy.order.alert_message}}||key=MYSECRETKEY||

ZIGNALY INTEGRATION - Webhook integration example

What you would write in your alert message:

{ {{strategy.order.alert_message}} , "key" : "MYSECRETKEY" }

CREDITS

I have reused and adapted some code from

'Directional Movement Index + ADX & Keylevel Support' study

which it's from TradingView console user.

I have reused and adapted some code from

'3ema' study

which it's from TradingView hunganhnguyen1193 user.

I have reused and adapted some code from

'Squeeze Momentum Indicator ' study

which it's from TradingView LazyBear user.

I have reused and adapted some code from

'Strategy Tester EMA-SMA-RSI-MACD' study

which it's from TradingView fikira user.

I have reused and adapted some code from

'Support Resistance MTF' study

which it's from TradingView LonesomeTheBlue user.

I have reused and adapted some code from

'TF Segmented Linear Regression' study

which it's from TradingView alexgrover user.

I have reused and adapted some code from

"Poor man's volume profile" study

which it's from TradingView IldarAkhmetgaleev user.

FEEDBACK

Please check the strategy source code for more detailed information

where, among others, I explain all of the substrats

and if they are implemented or not.

Q1. Did I understand wrong any of the Jaime substrats (which I have implemented)?

Q2. The strategy yields quite profit when we should long (EMA10 from 1d timeframe is higher than EMA55 from 1d timeframe.

Why the strategy yields much less profit when we should short (EMA10 from 1d timeframe is lower than EMA55 from 1d timeframe)?

Any idea if you need to do something else rather than just reverse what Jaime does when longing?

FREQUENTLY ASKED QUESTIONS

FAQ1. Why are you giving this strategy for free?

TradingLatino and his fellow enthusiasts taught me this strategy. Now I'm giving back to them.

FAQ2. Seriously! Why are you giving this strategy for free?

I'm confident his strategy might be improved a lot. By keeping it to myself I would avoid other people contributions to improve it.

Now that everyone can contribute this is a win-win.

FAQ3. How can I connect this strategy to my Exchange account?

It seems that you can attach alerts to strategies.

You might want to combine it with a paying account which enable Webhook URLs to work.

I don't know how all of this works right now so I cannot give you advice on it.

You will have to do your own research on this subject. But, be careful. Automating trades, if not done properly,

might end on you automating losses.

FAQ4. I have just found that this strategy by default gives more than 3.97% of 'maximum series of losses'. That's unacceptable according to my risk management policy.

You might want to reduce default stop loss setting from 7% to something like 5% till you are ok with the 'maximum series of losses'.

FAQ5. Where can I learn more about your work on this strategy?

Check the source code. You might find unused strategies. Either because there's not a substantial increases on earnings. Or maybe because they have not been implemented yet.

FAQ6. How much leverage is applied in this strategy?

No leverage.

FAQ7. Any difference with original Jaime Merino strategy?

Most of the times Jaime defines an stop loss at the price entry. That's not the case here. The default stop loss is 7% (but, don't be confused it only means losing 1% of your investment thanks to risk management). There's also a trailing take profit that triggers at 2% profit with a 1% trailing.

FAQ8. Why this strategy return is so small?

The strategy should be improved a lot. And, well, backtesting in this platform is not guaranteed to return theoric results comparable to real-life returns. That's why I'm personally forward testing this strategy to verify it.

MENSAJE EN CASTELLANO

En primer lugar se agradece feedback para mejorar la estrategia.

Si eres un usuario avanzado y quieres colaborar en mejorar el script no dudes en comentar abajo.

Ten en cuenta que aunque toda esta descripción tenga que estar en inglés no es obligatorio que el comentario esté en inglés.

CHISTE - CASTELLANO

¡Pero Jaime!

¡400.000!

¡Tu da mun!

Great Expectations [LucF]Great Expectations helps traders answer the question: What is possible? It is a powerful question, yet exploration of the unknown always entails risk. A more complete set of questions better suited to traders could be:

What opportunity exists from any given point on a chart?

What portion of this opportunity can be realistically captured?

What risk will be incurred in trying to do so, and how long will it take?

Great Expectations is the result of an exploration of these questions. It is a trade simulator that generates visual and quantitative information to help strategy modelers visually identify and analyse areas of optimal expectation on charts, whether they are designing automated or discretionary strategies.

WARNING: Great Expectations is NOT an indicator that helps determine the current state of a market. It works by looking at points in the past from which the future is already known. It uses one definition of repainting extensively (i.e. it goes back in the past to print information that could not have been know at the time). Repainting understood that way is in fact almost all the indicator does! —albeit for what I hope is a noble cause. The indicator is of no use whatsoever in analyzing markets in real-time. If you do not understand what it does, please stay away!

This is an indicator—not a strategy that uses TradingView’s backtesting engine. It works by simulating trades, not unlike a backtest, but with the crucial difference that it assumes a trade (either long or short) is entered on all bars in the historic sample. It walks forward from each bar and determines possible outcomes, gathering individual trade statistics that in turn generate precious global statistics from all outcomes tested on the chart.

Great Expectations provides numbers summarizing trade results on all simulations run from the chart. Those numbers cannot be compared to backtest-produced numbers since all non-filtered bars are examined, even if an entry was taken on the bar immediately preceding the current one, which never happens in a backtest. This peculiarity does NOT invalidate Great Expectations calculations; it just entails that results be considered under a different light. Provided they are evaluated within the indicator’s context, they can be useful—sometimes even more than backtesting results, e.g. in evaluating the impact of parameter-fitting or variations in entry, exit or filtering strats.

Traders and strategy modelers are creatures of hope often suffering from blurred vision; my hope is that Great Expectations will help them appraise the validity of their setup and strat intuitions in a realistic fashion, preventing confirmation bias from obstructing perspective—and great expectations from turning into financial great deceptions.

USE CASES

You’ve identified what looks like a promising setup on other indicators. You load Great Expectations on the chart and evaluate if its high-expectation areas match locations where your setup’s conditions occur. Unless today is your lucky day, chances are the indicator will help you realize your setup is not as promising as you had hoped.

You want to get a rough estimate of the optimal trade duration for a chart and you don’t mind using the entry and exit strategies provided with the indicator. You use the trade length readouts of the indicator.

You’re experimenting with a new stop strategy and want to know how long it will keep you in trades, on average. You integrate your stop strategy in the indicator’s code and look at the average trade length it produces and the TST ratio to evaluate its performance.

You have put together your own entry and exit criteria and are looking for a filter that will help you improve backtesting results. You visually ascertain the suitability of your filter by looking at its results on the charts with great Expectations, to see if your filter is choosing its areas correctly.

You have a strategy that shows backtested trades on your chart. Great Expectations can help you evaluate how well your strategy is benefitting from high-opportunity areas while avoiding poor expectation spots.

You want more complete statistics on your set of strategies than what backtesting will provide. You use Great Expectations, knowing that it tests all bars in the sample that correspond to your criteria, as opposed to backtesting results which are limited to a subset of all possible entries.

You want to fool your friends into thinking you’ve designed the holy grail of indicators, something that identifies optimal opportunities on any chart; you show them the P&L cloud.

FEATURES

For one trade

At any given point on the chart, assuming a trade is entered there, Great Expectations shows you information specific to that trade simulation both on the chart and in the Data Window.

The chart can display:

the P & L Cloud which shows whether the trade ended profitably or not, and by how much,

the Opportunity & Risk Cloud which the maximum opportunity and risk the simulation encountered. When superimposed over the P & L cloud, you will see what I call the managed opportunity and risk, i.e the portion of maximum opportunity that was captured and the portion of the maximum risk that was incurred,

the target and if it was reached,

a background that uses a gradient to show different levels of trade length, P&L or how frequently the target was reached during simulation.

The Data Window displays more than 40 values on individual trades and global results. For any given trade you will know:

Entry/Exit levels, including slippage impact,

It’s outcome and duration,

P/L achieved,

The fraction of the maximum opportunity/risk managed by the trade.

For all trades

After going through all the possible trades on the chart, the indicator will provide you with a rare view of all outcomes expressed with the P&L cloud, which allows us to instantly see the most/least profitable areas of a chart using trade data as support, while also showing its relationship with the opportunity/risk encountered during the simulation. The difference between the two clouds is the managed opportunity and risk.

The Data Window will present you with numbers which we will go through later. Some of them are: average stop size, P/L, win rate, % opportunity managed, trade lengths for different types of trade outcomes and the TST (Target:Stop Travel) ratio.

Let’s see Great Expectations in action… and remember to open your Data Window!

INPUTS

Trade direction : You must first choose if you wish to look at long or short trades. Because of the way the indicator works and the amount of visual information on the chart, it is only practical to look at one type of trades at a time. The default is Longs.

Maximum trade Length (MaxL) : This is the maximum walk forward distance the simulator will go in analyzing outcomes from any given point in the past. It also determines the size of the dead zone among the chart’s last bars. A red background line identifies the beginning of the dead zone for which not enough bars have elapsed to analyze outcomes for the maximum trade length defined. If an ATR-based entry stop is used, that length is added to the wait time before beginning simulations, so that the first entry starts with a clean ATR value. On a sample of around 16000 bars, my tests show that the indicator runs into server errors at lengths of around 290, i.e. having completed ~4,6M simulation loop iterations. That is way too high a length anyways; 100 will usually be amply enough to ring out all the possibilities out of a simulation, and on shorter time frames, 30 can be enough. While making it unduly small will prevent simulations of expressing the market’s potential, the less you use, the faster the indicator will run. The default is 40.

Unrealized P&L base at End of Trade (EOT) : When a simulation ends and the trade is still open, we calculate unrealized P&L from an exit order executed from either the last in-trade stop on the previous bar, or the close of the last bar. You can readily see the impact of this selection on the chart, with the P&L cloud. The default is on the close.

Display : The check box besides the title does nothing.

Show target : Shows a green line displaying the trade’s target expressed as a multiple of X, i.e. the amplitude of the entry stop. I call this value “X” and use it as a unit to express profit and loss on a trade (some call it “R”). The line is highlighted for trades where the close reached the target during the trade, whether the trade ended in profit or loss. This is also where you specify the multiple of X you wish to use in calculating targets. The multiple is used even if targets are not displayed.

Show P&L Cloud : The cloud allows traders to see right away the profitable areas of the chart. The only line printed with the cloud is the “end of trade line” (EOT). The EOT line is the only way one can see the level where a trade ended on the chart (in the Data Window you can see it as the “Exit Fill” value). The EOT level for the trade determines if the trade ended in a profit or a loss. Its value represents one of the following:

- fill from order executed at close of bar where stop is breached during trade (which produces “Realized P/L”),

- simulation of a fill pseudo-fill at the user-defined EOT level (last close or stop level) if the trade runs its course through MaxL bars without getting stopped (producing Unrealized P/L).

The EOT line and the cloud fill print in green when the trade’s outcome is profitable and in red when it is not. If the trade was closed after breaching the stop, the line appears brighter.

Show Opportunity&Risk Cloud : Displays the maximum opportunity/risk that was present during the trade, i.e. the maximum and minimum prices reached.

Background Color Scheme : Allows you to choose between 3 different color schemes for the background gradients, to accommodate different types of chart background/candles. Select “None” if you don’t want a background.

Background source : Determines what value will be used to generate the different intensities of the gradient. You can choose trade length (brighter is shorter), Trade P&L (brighter is higher) or the number of times the target was reached during simulation (brighter is higher). The default is Trade Length.

Entry strat : The check box besides the title does nothing. The default strat is All bars, meaning a trade will be simulated from all bars not excluded by the filters where a MaxL bars future exists. For fun, I’ve included a pseudo-random entry strat (an indirect way of changing the seed is to vary the starting date of the simulation).

Show Filter State : Displays areas where the combination of filters you have selected are allowing entries. Filtering occurs as per your selection(s), whether the state is displayed or not. The effect of multiple selections is additive. The filters are:

1. Bar direction: Longs will only be entered if close>open and vice versa.

2. Rising Volume: Applies to both long and shorts.

3. Rising/falling MA of the length you choose over the number of bars you choose.

4. Custom indicator: You can feed your own filtering signal through this from another indicator. It must produce a signal of 1 to allow long entries and 0 to allow shorts.

Show Entry Stops :

1. Multiple of user-defined length ATR.

2. Fixed percentage.

3. Fixed value.

All entry stops are calculated using the entry fill price as a reference. The fill price is calculated from the current bar’s open, to which slippage is added if configured. This simulates the case where the strategy issued the entry signal on the previous bar for it to be executed at the next bar’s open.

The entry stop remains active until the in-trade stop becomes the more aggressive of the two stops. From then on, the entry stop will be ignored, unless a bar close breaches the in-trade stop, in which case the stop will be reset with a new entry stop and the process repeats.

Show In-trade stops : Displays in bright red the selected in-trade stop (be sure to read the note in this section about them).

1. ATR multiple: added/subtracted from the average of the two previous bars minimum/maximum of open/close.

2. A trailing stop with a deviation expressed as a multiple of entry stop (X).

3. A fixed percentage trailing stop.

Trailing stops deviations are measured from the highest/lowest high/low reached during the trade.

Note: There is a twist with the in-trade stops. It’s that for any given bar, its in-trade stop can hold multiple values, as each successive pass of the advancing simulation loops goes over it from a different entry points. What is printed is the stop from the loop that ended on that bar, which may have nothing to do with other instances of the trade’s in-trade stop for the same bar when visited from other starting points in previous simulations. There is just no practical way to print all stop values that were used for any given bar. While the printed entry stops are the actual ones used on each bar, the in-trade stops shown are merely the last instance used among many.

Include Slippage : if checked, slippage will be added/subtracted from order price to yield the fill price. Slippage is in percentage. If you choose to include slippage in the simulations, remember to adjust it by considering the liquidity of the markets and the time frame you’ll be analyzing.

Include Fees : if checked, fees will be subtracted/added to both realized an unrealized trade profits/losses. Fees are in percentage. The default fees work well for crypto markets but will need adjusting for others—especially in Forex. Remember to modify them accordingly as they can have a major impact on results. Both fees and slippage are included to remind us of their importance, even if the global numbers produced by the indicator are not representative of a real trading scenario composed of sequential trades.

Date Range filtering : the usual. Just note that the checkbox has to be selected for date filtering to activate.

DATA WINDOW

Most of the information produced by this indicator is made available in the Data Window, which you bring up by using the icon below the Watchlist and Alerts buttons at the right of the TV UI. Here’s what’s there.

Some of the information presented in the Data Window is standard trade data; other values are not so standard; e. g. the notions of managed opportunity and risk and Target:Stop Travel ratio. The interplay between all the values provided by Great Expectations is inherently complex, even for a static set of entry/filter/exit strats. During the constant updating which the habitual process of progressive refinement in building strategies that is the lot of strategy modelers entails, another level of complexity is no doubt added to the analysis of this indicator’s values. While I don’t want to sound like Wolfram presenting A New Kind of Science , I do believe that if you are a serious strategy modeler and spend the time required to get used to using all the information this indicator makes available, you may find it useful.

Trade Information

Entry Order : This is the open of the bar where simulation starts. We suppose that an entry signal was generated at the previous bar.

Entry Fill (including slip.) : The actual entry price, including slippage. This is the base price from which other values will be calculated.

Exit Order : When a stop is breached, an exit order is executed from the close of the bar that breached the stop. While there is no “In-trade stop” value included in the Data Window (other than the End of trade Stop previously discussed), this “Exit Order” value is how we can know the level where the trade was stopped during the simulation. The “Trade Length” value will then show the bar where the stop was breached.

Exit Fill (including slip.) : When the exit order is simulated, slippage is added to the order level to create the fill.

Chart: Target : This is the target calculated at the beginning of the simulation. This value also appear on the chart in teal. It is controlled by the multiple of X defined under the “Show Target” checkbox in the Inputs.

Chart: Entry Stop : This value also appears on the chart (the red dots under points where a trade was simulated). Its value is controlled by the Entry Strat chosen in the Inputs.

X (% Fill, including Fees) and X (currency) : This is the stop’s amplitude (Entry Fill – Entry Stop) + Fees. It represents the risk incurred upon entry and will be used to express P&L. We will show R expressed in both a percentage of the Entry Fill level (this value), and currency (the next value). This value represents the risk in the risk:reward ratio and is considered to be a unit of 1 so that RR can be expressed as a single value (i.e. “2” actually meaning “1:2”).

Trade Length : If trade was stopped, it’s the number of bars elapsed until then. The trade is then considered “Closed”. If the trade ends without being stopped (there is no profit-taking strat implemented, so the stop is the only exit strat), then the trade is “Open”, the length is MaxL and it will show in orange. Otherwise the value will print in green/red to reflect if the trade is winning/losing.

P&L (X) : The P&L of the trade, expressed as a multiple of X, which takes into account fees paid at entry and exit. Given our default target setting at 2 units of “X”, a trade that closes at its target will have produced a P&L of +2.0, i.e. twice the value of X (not counting fees paid at exit ). A trade that gets stopped late 50% further that the entry stop’s level will produce a P&L of -1.5X.

P&L (currency, including Fees) : same value as above, but expressed in currency.

Target first reached at bar : If price closed above the target during the trade (even if it occurs after the trade was stopped), this will show when. This value will be used in calculating our TST ratio.

Times Stop/Target reached in sim. : Includes all occurrences during the complete simulation loop.

Opportunity (X) : The highest/lowest price reached during a simulation, i.e. the maximum opportunity encountered, whether the trade was previously stopped or not, expressed as a multiple of X.

Risk (X) : The lowest/highest price reached during a simulation, i.e. the maximum risk encountered, whether the trade was previously stopped or not, expressed as a multiple of X.

Risk:Opportunity : The greater this ratio, the greater Opportunity is, compared to Risk.

Managed Opportunity (%) : The portion of Opportunity that was captured by the highest/low stop position, even if it occurred after a previous stop closed the trade.

Managed Risk (%) : The portion of risk that was protected by the lowest/highest stop position, even if it occurred after a previous stop closed the trade. When this value is greater than 100%, it means the trade’s stop is protecting more than the maximum risk, which is frequent. You will, however, never see close to those values for the Managed Opportunity value, since the stop would have to be higher than the Maximum opportunity. It is much easier to alleviate the risk than it is to lock in profits.

Managed Risk:Opportunity : The ratio of the two preceding values.

Managed Opp. vs. Risk : The Managed Opportunity minus the Managed Risk. When it is negative, which is most often is, it means your strat is protecting a greater portion of the risk than it captures opportunity.

Global Numbers

Win Rate(%) : Percentage of winning trades over all entries. Open trades are considered winning if their last stop/close (as per user selection) locks in profits.

Avg X%, Avg X (currency) : Averages of previously described values:.

Avg Profitability/Trade (APPT) : This measures expectation using: Average Profitability Per Trade = (Probability of Win × Average Win) − (Probability of Loss × Average Loss) . It quantifies the average expectation/trade, which RR alone can’t do, as the probabilities of each outcome (win/lose) must also be used to calculate expectancy. The APPT combine the RR with the win rate to yield the true expectancy of a strategy. In my usual way of expressing risk with X, APPT is the equivalent of the average P&L per trade expressed in X. An APPT of -1.5 means that we lose on average 1.5X/trade.

Equity (X), Equity (currency) : The cumulative result of all trade outcomes, expressed as a multiple of X. Multiplied by the Average X in currency, this yields the Equity in currency.

Risk:Opportunity, Managed Risk:Opportunity, Managed Opp. vs. Risk : The global values of the ones previously described.

Avg Trade Length (TL) : One of the most important values derived by going through all the simulations. Again, it is composed of either the length of stopped trades, or MaxL when the trade isn’t stopped (open). This value can help systems modelers shape the characteristics of the components they use to build their strategies.

Avg Closed Win TL and Avg Closed Lose TL : The average lengths of winning/losing trades that were stopped.

Target reached? Avg bars to Stop and Target reached? Avg bars to Target : For the trades where the target was reached at some point in the simulation, the number of bars to the first point where the stop was breached and where the target was reached, respectively. These two values are used to calculate the next value.

TST (Target:Stop Travel Ratio) : This tracks the ratio between the two preceding values (Bars to first stop/Bars to first target), but only for trades where the target was reached somewhere in the loop. A ratio of 2 means targets are reached twice as fast as stops.

The next values of this section are counts or percentages and are self-explanatory.

Chart Plots

Contains chart plots of values already describes.

NOTES

Optimization/Overfitting: There is a fine line between optimizing and overfitting. Tools like this indicator can lead unsuspecting modelers down a path of overfitting that often turns strategies into over-specialized beasts that do not perform elegantly when confronted to the real-world. Proven testing strategies like walk forward analysis will go a long way in helping modelers alleviate this risk.

Input tuning: Because the results generated by the indicator will vary with the parameters used in the active entry, filtering and exit strats, it’s important to realize that although it may be fun at first, just slapping the default settings on a chart and time frame will not yield optimal nor reliable results. While using ATR as often as possible (as I do in this indicator) is a good way to make strat parametrization adaptable, it is not a foolproof solution.

There is no data for the last MaxL bars of the chart, since not enough trade future has elapsed to run a simulation from MaxL bars back.

Modifying the code: I have tried to structure the code modularly, even if that entails a larger code base, so that you can adapt it to your needs. I’ve included a few token components in each of the placeholders designed for entry strategies, filters, entry stops and in-trade stops. This will hopefully make it easier to add your own. In the same spirit, I have also commented liberally.

You will find in the code many instances of standard trade management tasks that can be lifted to code TV strategies where, as I do in mine, you manage everything yourself and don’t rely on built-in Pine strategy functions to act on your trades.

Enjoy!

THANKS

To @scarf who showed me how plotchar() could be used to plot values without ruining scale.

To @glaz for the suggestion to include a Chandelier stop strat; I will.

To @simpelyfe for the idea of using an indicator input for the filters (if some day TV lets us use more than one, it will be useful in other modules of the indicator).

To @RicardoSantos for the random generator used in the random entry strat.

To all scripters publishing open source on TradingView; their code is the best way to learn.

To my trading buddies Irving and Bruno; who showed me way back how pro traders get it done.

BOCS AdaptiveBOCS Adaptive Strategy - Automated Volatility Breakout System

WHAT THIS STRATEGY DOES:

This is an automated trading strategy that detects consolidation patterns through volatility analysis and executes trades when price breaks out of these channels. Take-profit and stop-loss levels are calculated dynamically using Average True Range (ATR) to adapt to current market volatility. The strategy closes positions partially at the first profit target and exits the remainder at the second target or stop loss.

TECHNICAL METHODOLOGY:

Price Normalization Process:

The strategy begins by normalizing price to create a consistent measurement scale. It calculates the highest high and lowest low over a user-defined lookback period (default 100 bars). The current close price is then normalized using the formula: (close - lowest_low) / (highest_high - lowest_low). This produces values between 0 and 1, allowing volatility analysis to work consistently across different instruments and price levels.

Volatility Detection:

A 14-period standard deviation is applied to the normalized price series. Standard deviation measures how much prices deviate from their average - higher values indicate volatility expansion, lower values indicate consolidation. The strategy uses ta.highestbars() and ta.lowestbars() functions to track when volatility reaches peaks and troughs over the detection length period (default 14 bars).

Channel Formation Logic:

When volatility crosses from a high level to a low level, this signals the beginning of a consolidation phase. The strategy records this moment using ta.crossover(upper, lower) and begins tracking the highest and lowest prices during the consolidation. These become the channel boundaries. The duration between the crossover and current bar must exceed 10 bars minimum to avoid false channels from brief volatility spikes. Channels are drawn using box objects with the recorded high/low boundaries.

Breakout Signal Generation:

Two detection modes are available:

Strong Closes Mode (default): Breakout occurs when the candle body midpoint math.avg(close, open) exceeds the channel boundary. This filters out wick-only breaks.

Any Touch Mode: Breakout occurs when the close price exceeds the boundary.

When price closes above the upper channel boundary, a bullish breakout signal generates. When price closes below the lower boundary, a bearish breakout signal generates. The channel is then removed from the chart.

ATR-Based Risk Management:

The strategy uses request.security() to fetch ATR values from a specified timeframe, which can differ from the chart timeframe. For example, on a 5-minute chart, you can use 1-minute ATR for more responsive calculations. The ATR is calculated using ta.atr(length) with a user-defined period (default 14).

Exit levels are calculated at the moment of breakout:

Long Entry Price = Upper channel boundary

Long TP1 = Entry + (ATR × TP1 Multiplier)

Long TP2 = Entry + (ATR × TP2 Multiplier)

Long SL = Entry - (ATR × SL Multiplier)

For short trades, the calculation inverts:

Short Entry Price = Lower channel boundary

Short TP1 = Entry - (ATR × TP1 Multiplier)

Short TP2 = Entry - (ATR × TP2 Multiplier)

Short SL = Entry + (ATR × SL Multiplier)

Trade Execution Logic:

When a breakout occurs, the strategy checks if trading hours filter is satisfied (if enabled) and if position size equals zero (no existing position). If volume confirmation is enabled, it also verifies that current volume exceeds 1.2 times the 20-period simple moving average.

If all conditions are met:

strategy.entry() opens a position using the user-defined number of contracts

strategy.exit() immediately places a stop loss order

The code monitors price against TP1 and TP2 levels on each bar

When price reaches TP1, strategy.close() closes the specified number of contracts (e.g., if you enter with 3 contracts and set TP1 close to 1, it closes 1 contract). When price reaches TP2, it closes all remaining contracts. If stop loss is hit first, the entire position exits via the strategy.exit() order.

Volume Analysis System:

The strategy uses ta.requestUpAndDownVolume(timeframe) to fetch up volume, down volume, and volume delta from a specified timeframe. Three display modes are available:

Volume Mode: Shows total volume as bars scaled relative to the 20-period average

Comparison Mode: Shows up volume and down volume as separate bars above/below the channel midline

Delta Mode: Shows net volume delta (up volume - down volume) as bars, positive values above midline, negative below

The volume confirmation logic compares breakout bar volume to the 20-period SMA. If volume ÷ average > 1.2, the breakout is classified as "confirmed." When volume confirmation is enabled in settings, only confirmed breakouts generate trades.

INPUT PARAMETERS:

Strategy Settings:

Number of Contracts: Fixed quantity to trade per signal (1-1000)

Require Volume Confirmation: Toggle to only trade signals with volume >120% of average

TP1 Close Contracts: Exact number of contracts to close at first target (1-1000)

Use Trading Hours Filter: Toggle to restrict trading to specified session

Trading Hours: Session input in HHMM-HHMM format (e.g., "0930-1600")

Main Settings:

Normalization Length: Lookback bars for high/low calculation (1-500, default 100)

Box Detection Length: Period for volatility peak/trough detection (1-100, default 14)

Strong Closes Only: Toggle between body midpoint vs close price for breakout detection

Nested Channels: Allow multiple overlapping channels vs single channel at a time

ATR TP/SL Settings:

ATR Timeframe: Source timeframe for ATR calculation (1, 5, 15, 60, etc.)

ATR Length: Smoothing period for ATR (1-100, default 14)

Take Profit 1 Multiplier: Distance from entry as multiple of ATR (0.1-10.0, default 2.0)

Take Profit 2 Multiplier: Distance from entry as multiple of ATR (0.1-10.0, default 3.0)

Stop Loss Multiplier: Distance from entry as multiple of ATR (0.1-10.0, default 1.0)

Enable Take Profit 2: Toggle second profit target on/off

VISUAL INDICATORS:

Channel boxes with semi-transparent fill showing consolidation zones

Green/red colored zones at channel boundaries indicating breakout areas

Volume bars displayed within channels using selected mode

TP/SL lines with labels showing both price level and distance in points

Entry signals marked with up/down triangles at breakout price

Strategy status table showing position, contracts, P&L, ATR values, and volume confirmation status

HOW TO USE:

For 2-Minute Scalping:

Set ATR Timeframe to "1" (1-minute), ATR Length to 12, TP1 Multiplier to 2.0, TP2 Multiplier to 3.0, SL Multiplier to 1.5. Enable volume confirmation and strong closes only. Use trading hours filter to avoid low-volume periods.

For 5-15 Minute Day Trading:

Set ATR Timeframe to match chart or use 5-minute, ATR Length to 14, TP1 Multiplier to 2.0, TP2 Multiplier to 3.5, SL Multiplier to 1.2. Volume confirmation recommended but optional.

For Hourly+ Swing Trading:

Set ATR Timeframe to 15-30 minute, ATR Length to 14-21, TP1 Multiplier to 2.5, TP2 Multiplier to 4.0, SL Multiplier to 1.5. Volume confirmation optional, nested channels can be enabled for multiple setups.

BACKTEST CONSIDERATIONS:

Strategy performs best during trending or volatility expansion phases

Consolidation-heavy or choppy markets produce more false signals

Shorter timeframes require wider stop loss multipliers due to noise

Commission and slippage significantly impact performance on sub-5-minute charts

Volume confirmation generally improves win rate but reduces trade frequency

ATR multipliers should be optimized for specific instrument characteristics

COMPATIBLE MARKETS:

Works on any instrument with price and volume data including forex pairs, stock indices, individual stocks, cryptocurrency, commodities, and futures contracts. Requires TradingView data feed that includes volume for volume confirmation features to function.

KNOWN LIMITATIONS:

Stop losses execute via strategy.exit() and may not fill at exact levels during gaps or extreme volatility

request.security() on lower timeframes requires higher-tier TradingView subscription

False breakouts inherent to breakout strategies cannot be completely eliminated

Performance varies significantly based on market regime (trending vs ranging)

Partial closing logic requires sufficient position size relative to TP1 close contracts setting

RISK DISCLOSURE:

Trading involves substantial risk of loss. Past performance of this or any strategy does not guarantee future results. This strategy is provided for educational purposes and automated backtesting. Thoroughly test on historical data and paper trade before risking real capital. Market conditions change and strategies that worked historically may fail in the future. Use appropriate position sizing and never risk more than you can afford to lose. Consider consulting a licensed financial advisor before making trading decisions.

ACKNOWLEDGMENT & CREDITS:

This strategy is built upon the channel detection methodology created by AlgoAlpha in the "Smart Money Breakout Channels" indicator. Full credit and appreciation to AlgoAlpha for pioneering the normalized volatility approach to identifying consolidation patterns and sharing this innovative technique with the TradingView community. The enhancements added to the original concept include automated trade execution, multi-timeframe ATR-based risk management, partial position closing by contract count, volume confirmation filtering, and real-time position monitoring.

The Best Strategy Template[LuciTech]Hello Traders,

This is a powerful and flexible strategy template designed to help you create, backtest, and deploy your own custom trading strategies. This template is not a ready-to-use strategy but a framework that simplifies the development process by providing a wide range of pre-built features and functionalities.

What It Does

The LuciTech Strategy Template provides a robust foundation for building your own automated trading strategies. It includes a comprehensive set of features that are essential for any serious trading strategy, allowing you to focus on your unique trading logic without having to code everything from scratch.

Key Features

The LuciTech Strategy Template integrates several powerful features to enhance your strategy development:

•

Advanced Risk Management: This includes robust controls for defining your Risk Percentage per Trade, setting a precise Risk-to-Reward Ratio, and implementing an intelligent Breakeven Stop-Loss mechanism that automatically adjusts your stop to the entry price once a specified profit threshold is reached. These elements are crucial for capital preservation and consistent profitability.

•

Flexible Stop-Loss Options: The template offers adaptable stop-loss calculation methods, allowing you to choose between ATR-Based Stop-Loss, which dynamically adjusts to market volatility, and Candle-Based Stop-Loss, which uses structural price points from previous candles. This flexibility ensures the stop-loss strategy aligns with diverse trading styles.

•

Time-Based Filtering: Optimize your strategy's performance by restricting trading activity to specific hours of the day. This feature allows you to avoid unfavorable market conditions or focus on periods of higher liquidity and volatility relevant to your strategy.

•

Customizable Webhook Alerts: Stay informed with advanced notification capabilities. The template supports sending detailed webhook alerts in various JSON formats (Standard, Telegram, Concise Telegram) to external platforms, facilitating real-time monitoring and potential integration with automated trading systems.

•

Comprehensive Visual Customization: Enhance your analytical clarity with extensive visual options. You can customize the colors of entry, stop-loss, and take-profit lines, and effectively visualize market inefficiencies by displaying and customizing Fair Value Gap (FVG) boxes directly on your chart.

How It Does It

The LuciTech Strategy Template is meticulously crafted using Pine Script, TradingView's powerful and expressive programming language. The underlying architecture is designed for clarity and modularity, allowing for straightforward integration of your unique trading signals. At its core, the template operates by taking user-defined entry and exit conditions and then applying a sophisticated layer of risk management, position sizing, and trade execution logic.

For instance, when a longCondition or shortCondition is met, the template dynamically calculates the appropriate position size. This calculation is based on your specified risk_percent of equity and the stop_distance (the distance between your entry price and the calculated stop-loss level). This ensures that each trade adheres to your predefined risk parameters, a critical component of disciplined trading.

The flexibility in stop-loss calculation is achieved through a switch statement that evaluates the sl_type input. Whether you choose an ATR-based stop, which adapts to market volatility, or a candle-based stop, which uses structural price points, the template seamlessly integrates these methods. The ATR calculation itself is further refined by allowing various smoothing methods (RMA, SMA, EMA, WMA), providing granular control over how volatility is measured.

Time-based filtering is implemented by comparing the current bar's time with user-defined start_hour, start_minute, end_hour, and end_minute inputs. This allows the strategy to activate or deactivate trading during specific market sessions or periods of the day, a valuable tool for optimizing performance and avoiding unfavorable conditions.

Furthermore, the template incorporates advanced webhook alert functionality. When a trade is executed, a customizable JSON message is formatted based on your webhook_format selection (Standard, Telegram, or Concise Telegram) and sent via alert function. This enables seamless integration with external services for real-time notifications or even automated trade execution through third-party platforms.

Visual feedback is paramount for understanding strategy behavior. The template utilizes plot and fill functions to clearly display entry prices, stop-loss levels, and take-profit targets directly on the chart. Customizable colors for these elements, along with dedicated options for Fair Value Gap (FVG) boxes, enhance the visual analysis during backtesting and live trading, making it easier to interpret the strategy's actions.

How It's Original

The LuciTech Strategy Template distinguishes itself in the crowded landscape of TradingView scripts through its unique combination of integrated, advanced risk management features, highly flexible stop-loss methodologies, and sophisticated alerting capabilities, all within a user-friendly and modular framework. While many templates offer basic entry/exit signal integration, LuciTech goes several steps further by providing a robust, ready-to-use infrastructure for managing the entire trade lifecycle once a signal is generated.

Unlike templates that might require users to piece together various risk management components or code complex stop-loss logic from scratch, LuciTech offers these critical functionalities out-of-the-box. The inclusion of dynamic position sizing based on a user-defined risk percentage, a configurable risk-to-reward ratio, and an intelligent breakeven mechanism significantly elevates its utility. This comprehensive approach to capital preservation and profit targeting is a cornerstone of professional trading and is often overlooked or simplified in generic templates.

Furthermore, the template's provision for multiple stop-loss calculation types—ATR-based for volatility adaptation, and candle-based for structural support/resistance—demonstrates a deep understanding of diverse trading strategies. The underlying code for these calculations is already implemented, saving developers considerable time and effort. The subtle yet powerful inclusion of FVG (Fair Value Gap) related inputs also hints at advanced price action concepts, offering a sophisticated layer of analysis and execution that is not commonly found in general-purpose templates.

The advanced webhook alerting system, with its support for various JSON formats tailored for platforms like Telegram, showcases an originality in catering to the needs of modern, automated trading setups. This moves beyond simple TradingView pop-up alerts, enabling seamless integration with external systems for real-time trade monitoring and execution. This level of external connectivity and customizable data output is a significant differentiator.

In essence, the LuciTech Strategy Template is original not just in its individual features, but in how these features are cohesively integrated to form a powerful, opinionated, yet highly adaptable system. It empowers traders to focus their creative energy on developing their core entry/exit signals, confident that the underlying framework will handle the complexities of risk management, trade execution, and external communication with precision and flexibility. It's a comprehensive solution designed to accelerate the development of robust and professional trading strategies.

How to Modify the Logic to Apply Your Strategy

The LuciTech Strategy Template is designed with modularity in mind, making it exceptionally straightforward to integrate your unique trading strategy logic. The template provides a clear separation between the core strategy management (risk, position sizing, exits) and the entry signal generation. This allows you to easily plug in your own buy and sell conditions without altering the robust underlying framework.

Here’s a step-by-step guide on how to adapt the template to your specific trading strategy:

1.

Locate the Strategy Logic Section:

Open the Pine Script editor in TradingView and navigate to the section clearly marked with the comment //Strategy Logic Example:. This is where the template’s placeholder entry conditions (a simple moving average crossover) are defined.

2.

Define Your Custom Entry Conditions:

Within this section, you will find variables such as longCondition and shortCondition. These are boolean variables that determine when a long or short trade should be initiated. Replace the existing example logic with your own custom buy and sell conditions. Your conditions can be based on any combination of indicators, price action patterns, candlestick formations, or other market analysis techniques. For example, if your strategy involves a combination of RSI and MACD, you would define longCondition as (rsi > 50 and macd_line > signal_line) and shortCondition as (rsi < 50 and macd_line < signal_line).

3.